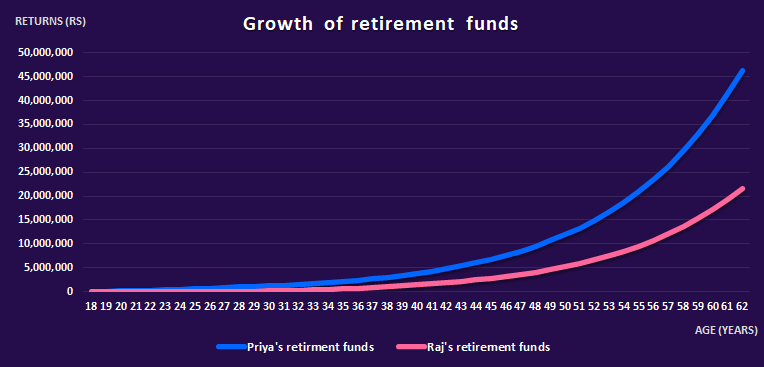

Compound interest is a powerful tool that can increase any initial capital at staggering rates as long as the time period is significant enough. Imagine two friends, Priya and Raj. Priya wanted to start her investment journey early and set aside Rs 50,000 for 10 years, between the ages of 18 to 28, to create a retirement fund. Raj thought 18 is too early to start investing. He wanted to get settled in a stable job before making any such commitments. Hence, Raj started at 28 and continued to invest Rs 50,000 towards his retirement fund all the way till he retired at age 62. Assuming a 12% annual return in both cases, let’s see how both of them fared.

- Priya:

- Total amount invested = Rs 5,00,000

- Size of retirement fund = Rs 4,63,28,327

- Raj:

- Total amount invested = Rs 17,50,000

- Total returns received at retirement = Rs 2,15,83,175