Key Takeaways

- An adequate estate plan will include all details on how one’s assets should be preserved, managed and distributed upon their demise.

- Life insurance proceeds are the fastest way of getting access to cash payouts which are crucial to settle any outstanding debt, taxes and other immediate expenses such as funeral arrangements.

- Life insurance helps to even out the assets that differ significantly in value so that none of the beneficiaries are shortchanged in what they receive.

- Instead of hoarding all the wealth, set aside a small portion of your income into life insurance and enjoy the lifestyle you deserve with the peace of mind that your insurance will provide sufficient support to your family upon death.

In our recent posts, we have discussed why estate planning is critical for everyone, and the benefits we derive from having an adequate estate plan. The question now is, how do we make arrangements for all of our wealth that we worked so hard for, to go to our loved ones and to the causes we care about? What can be the least painful and hassle-free manner to bring this idea to fruition? While each individual will have their own way to go about it based on their own requirements, we must first understand what steps are involved in estate planning and then chart out the best suited plan for our own needs.

How to go about Estate Planning?

An adequate estate plan will include all details on how one’s assets should be preserved, managed and distributed upon their demise. Of course, all these details need to continue being updated in line with changes in one’s life, such as acquisition of new assets, inclusion of new beneficiaries (upon marriage and having kids), and so on.

Generally speaking, estate planning may involve, in no particular sequence, setting up a trust, writing up a will, assigning a trustee (for the trust) and an executor (of a will), establishing joint ownership of assets and liabilities, formulating power of attorney and getting life insurance. Each of these components vary in terms of the purpose they serve, the resources needed and the processes involved. Hence, it only makes sense to tend to one topic at a time.

Importance of Life Insurance in Estate Planning

In today’s post, we’ll be focusing on one of the more straightforward topics – life insurance. Although it may seem to serve the sole purpose of meeting the needs of your loved ones post your demise, it is actually a key component of your estate planning. Let’s understand its role in more detail.

Immediate cash to settle outstanding liabilities

Life insurance proceeds are the fastest way of getting access to cash payouts which are crucial to settle any outstanding debt, taxes and other immediate expenses such as funeral arrangements. This provides the family some time to figure out distribution of other assets whether or not a will is in place. Usually, execution of a will could take up to a few months. Moreover, the liquid cash in the bank accounts are frozen upon a person’s death – only to be released according to instructions in a will, or relevant succession act (which may be based on the deceased’s religion or Indian Succession Act 1925) in the absence of a will. In such cases, a life insurance claim is a huge relief for a grieving family who need to take over and manage all the financial matters.

Even distribution of wealth

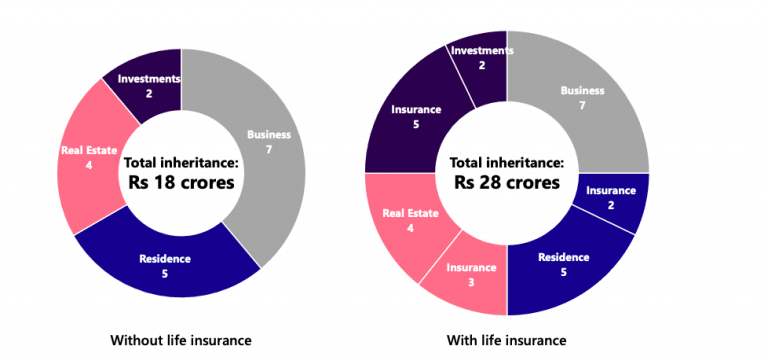

Life insurance helps to even out the assets that differ significantly in value so that none of the beneficiaries are shortchanged in what they receive. Let’s say a businessman owns a company (worth Rs 7 crores), a residential property (worth Rs 5 crores) and an investment property (worth Rs 4 crores), along with some liquid investments (say Rs 2 crores). If the person wants to divide these equally amongst his 4 beneficiaries, first of all the business and properties will need to be liquidated, and only then can the proceeds be divided accordingly. Not only will it be a tedious process, but will also be subject to market volatility, which could mean that one may not get a fair value for the asset. In such a case, if the individual has say a life insurance worth Rs 10 crore, it can be split such that the assets of lesser value (Rs 5, 4 and 2 crores) can be supplemented in order to match up to the one with the highest value (Rs 7 crores), such that each of the beneficiaries end up with an equal inheritance worth Rs 7 crores.

Enhancing the inheritance amount

The challenge of limited resources and unlimited needs is no different when it comes to planning our legacy. The portion of our income and wealth that we consume in our lifetime directly impacts the bequest amount that we leave behind. Should we then compromise on our lifestyle so that we can leave behind a bigger inheritance in the interest of our family members? Thankfully, there is a better way. Instead of hoarding all the wealth, set aside a small portion of your income into life insurance and enjoy the lifestyle you deserve with the peace of mind that your insurance will provide sufficient support to your family upon death. As illustrated in the earlier example of the businessman, the inheritance sum was enhanced from 18 crores to 28 crores with the use of life insurance.

Bottom Line

Life insurance proceeds can form a significant chunk of your estate. Not only is it an essential part of estate planning, it’s also one of the easiest steps to get started with. To lay the right foundation for your estate plan, buy an appropriate insurance plan that meets your family’s needs, upgrade your coverage with changing life stages and keep your nominations up to date.

With Cashvisory, you will be able to plan for your insurance needs and manage these plans all in one place. Stay tuned to learn more on the other topics related to estate planning, and how we can help you with those!