Solvency Ratio = (Net Worth / Assets) x 100

Example: Let us say Raj has the following financials:

Assets:

- Home: Rs 50,00,000

- Investments: Rs 20,00,000

- Cash: Rs 5,00,000

Total Assets = Rs 75,00,000

Liabilities:

- Mortgage: Rs 30,00,000

- Car loan: Rs 2,00,000

- Credit card loan: Rs 1,00,000

Total Liabilities = Rs 33,00,000

Net Worth = Total Assets – Total Liabilities = Rs 42,00,000

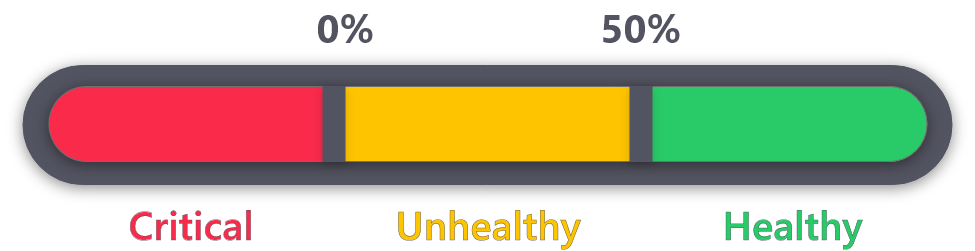

Solvency Ratio = (42,00,000 / 75,00,000) x 100 = 56%